Workstation for trade supply & demand details incoming or outgoing inventory to a specific order.

FINANCIAL ACCOUNTING

PORTFOLIOS

GROUP ESTATES

No.:

AI085

Issued Date:

Wed, Dec 14, 2005

Due Date:

Thu, Jul 1, 2010

Sat, May 1, 2010 Invitation with the contractor quotation.

ClientIdentifier customer

55 Riverside Ave

Provincial, AA Postal number

317-722-5066

ContractorIdentifier licensed teleworker

55262 A French Rd

Provincial, AA Postal number

317-234-1135

TraderFinancial environment framework

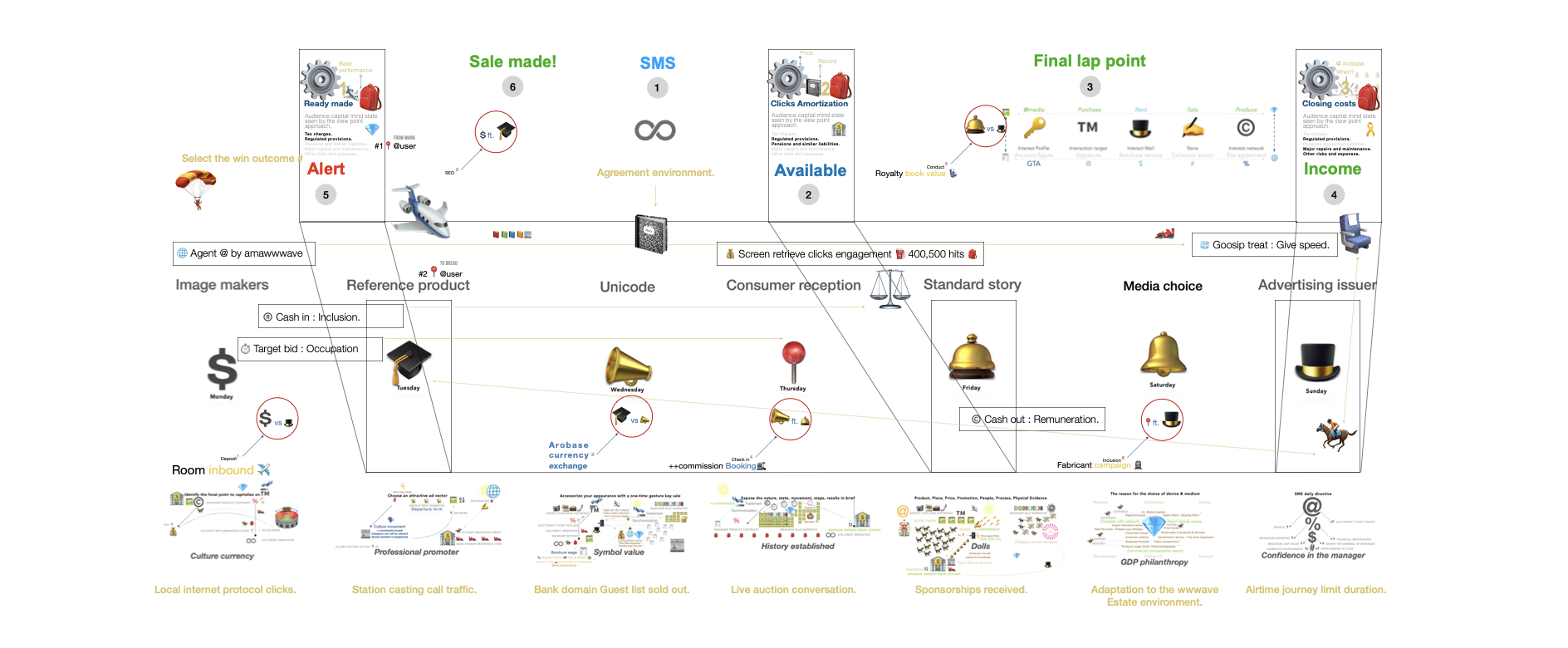

Agent welcome the client. Manager create an Allure GOOSIP for the client wwwave. Client choose an documentary narrative for the added link (None playable contract from the agency) to distribute and retrieve deposit/cash out. Sponsor call (are in advertising from Allure main style figure creator main domain investors) with the narrative bid and news development. Gross domestic product are in a precise selection date for the box office/trading networks (props and materials) integration. Multimedia news drive made by the agency from the platform alignments (identifier registered in wwwave) for and industrial update. Cash out recipe are sent by managers in wwwave, from the bank domain link available after industrial update. Deposit tax are sent to the agency by managers for an wwwave control continuation by the agency tax account owner. Christian Ndela Ngamwanya confirmation place to the Canadian Industry Statistics.

Barcode reprint.

DESCRIPTION

LABOR HOURS

RATE/COST

TOTAL

Subtotal$0.00

Agent (User profits for 4 Dataset Bundle)

12.0%$0.00

Tax$0.00$ 12

Total Due $0.00

Terms and Conditions:

1. Customer will be billed after indicating acceptance of this quote.

2. Payment will be due prior to delivery or the receptive of service and goods.

3. Please fax or mail the signed contractual terms allowing your portfolios administration price quote to the address above.

The Studio funds its internal productions. Any private luxuries (jets, suites) must be logged at full commercial rate in the ledger.

2. ENTITY BOUNDARIES (Rules)

If the Studio provides special resources to one lead auditioning, they must provide the same to every other hopeful.

1. TRADERS BUNDLE (Deposit Margin)

The Bundle serves as a security that pays periodic interest. Total interest accrued is returned from the issue date; individual points are redeemable for industrial services or products from authorized distributors.

2. NEW CLIENT VALUATION (Tiers)

Valuation follows the Group Fourth Round hierarchy. Industrial payouts are structured at $2,250 (Tier 4), $1,500 (Tier 3), $750 (Tier 2), and $3,000 (Venture Total). Secondary bonuses scale from $270 to $750 based on operational performance.

3. VENTURE AMORTIZATION (Rules)

Clearing benefits must be recorded as a one-time video record. Completion of the fourth brochure template triggers Venture Amortization, permitting the selection of a new domain for the trading station.

Verify Maturity Assets

Terminal Asset

Bench Rate

Tax Scenario

Total Yield

CONSOLIDATED TRADER MARGIN (2026):

$1,850.00

Departure: Customer Experience File

TRADE | SET YOUR COLISEUM SETTLEMENT

EARNINGS FINALITY

TERMINAL ASSET

BENCH RATE

TAX (%)

TOTAL YIELD

CONSOLIDATE YOUR PNR MARGIN:

$0.00

⛽️

@

%

$

#

@

%

$

#

🌎 🌍 🌏 Allure media 🪐 🌕 ☀️

Currency exchange betting ground.

Current distribution update: Jan 1 2022

🏎 Lantern Festival 🖼 60,001.100 💎

🌎 🌍 🌏 WWWAVE 🪐 🌕 ☀️

⛽️

Amass

Core Pooling Structures

Slate Financing: Multi-project capital diversification.

Co-Production: Shared risk on tentpole blockbusters.

SPV Investment: Private equity ring-fencing.

Pre-Sales: Using global licenses as debt collateral.

Financial Management

Recoupment: The "120 and 50" waterfall hierarchy.

Accounting: Managing net-profit via legal entity isolation.

Incentives: Aggregating global tax rebates and grants.

Modern Shifts: Moving from balance-sheet to partner funding.

AMA System Leading index • Main collective of users & Trendsetters through Advanced Network Control.

Slate Financing: Multi-project capital diversification.

Co-Production: Shared risk on tentpole blockbusters.

SPV Investment: Private equity ring-fencing.

Pre-Sales: Using global licenses as debt collateral.

Financial Management

Recoupment: The "120 and 50" waterfall hierarchy.

Accounting: Managing net-profit via legal entity isolation.

Incentives: Aggregating global tax rebates and grants.

Modern Shifts: Moving from balance-sheet to partner funding.

Seed: Cost Per Lead (CPL): Reducing the cost of acquiring new leads. • Growth: Ensuring ad spend leads to measurable revenue rather than just empty clicks. • Exit: Bond consolidation.

Slate Financing: Multi-project capital diversification.

Co-Production: Shared risk on tentpole blockbusters.

SPV Investment: Private equity ring-fencing.

Pre-Sales: Using global licenses as debt collateral.

Financial Management

Recoupment: The "120 and 50" waterfall hierarchy.

Accounting: Managing net-profit via legal entity isolation.

Incentives: Aggregating global tax rebates and grants.

Modern Shifts: Moving from balance-sheet to partner funding.

A curated catalog is a thoughtfully selected and organized collection of items, data, or resources designed to provide a high-quality, focused experience for a specific audience. • Curated catalog filters out the noise to showcase only the most relevant, vetted, or high-value items.

I. ADVISOR & ASSET IDENTIFICATION

Title: The Residential Strategist [J-01]

Asset: Municipal Infrastructure

Lookup: ICANN-Detained Service Consolidation

II. PERFORMANCE CERTIFICATION

Benchmark: 6.6% (Spread over Can-T Bills)

Alpha: Certified via Strategic Hedging

Status: Tier-1 Payout Grid Eligible

This document confirms that the Liquidation Value of the assets aligns with the Debt Obligation. Funding liquidity remains intact via professional hedging.

Jurisdictional Note: Canada trade secret protection is governed by Common Law/Civil Law (Quebec) via breach of confidence and fiduciary duty.

In essence, market circulation ensures that the money spent by one agent (e.g., a household buying groceries) becomes the income of another (e.g., a firm), which is then redistributed as wages or reinvested.

Allure Media Service Framework

System Launch & Operations

Managing an "Allure" account begins with a commercial and theatrical production launch, initiating commission-based traffic. This sequence progresses as productive time is purchased from commissioners through sample distribution hours intended for reproduction.

Thus, the entry into the "Narrative Allure" facilitates the visitor's circulation campaign. In cases where visit interactions are compensated, the visitor is paid via a commission placed by a commissioner listed within the domain bank registry.

Credit & Ownership

Station time is governed by the copyright assessment table. Managers, using tax numbers provided by Allure Media founder Christian Ndela Ngamwanya, register all involved parties as station owners. This is a private, bespoke service governed by the "Registered Allure"—a modifiable HTML file organized by both online and offline algorithms.

Allotment & Financial Flow

Following your registration confirmation between the service provider and the client (including distribution rights on the "wwwave" space), you may organize your financial flows. Your products and services are enumerated and aligned with the narratives of other "passengers."

Confirmed contracts allow the brochure to offer international station-hour rental services, independent of other days. These are included in an all-inclusive fixed-price package; this separation of activities is designed to facilitate total amortization.

Stats & Interaction

Statistics are real-time, reflecting daily activities organized by the station owner. Electronic signatures are updated via managed QR codes to indicate specific purchases within the current narrative. Product knowledge enables collective interaction following the directives of a brand or merchant, driving the economic progress of the Allure station through narrative milestones.

Management & Performance

Please select an economic figure manager; this agent will evaluate your performance based on the figures presented within the station. Consequently, profitability and competitiveness align with the same narrative structure purchased and leased by the station’s visiting audience.

Your financial deposits are processed through the holder of the Allure Media station's commercial hour rights, and your performance objectives are overseen by management.

🏎 WWWWTitle 🖼️ 5,000,001.700 💎

🌎 🌍 🌏 WWWAVE 🪐 🌕 ☀️

⛽️

Amass

Film Industry Financial Pooling

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

🛎 Motorcade

⚡️🔑 Statement & undergarment character mold set wwwave

Canada - River

⚡️🔑 Statement & undergarment character mold set wwwave

Greece

⚡️🔑 Statement & undergarment character mold set wwwave

Chile

⚡️🔑 Statement & undergarment character mold set wwwave

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

🛎 Motorcade

⚡️🔑 Fragrance vs. Flavor: The Art of the Wearable vs. the Edible set wwwave

Colombia - Bogotá and the Amazon

⚡️🔑 Fragrance vs. Flavor: The Art of the Wearable vs. the Edible set wwwave

Egypt - Cairo

⚡️🔑 Fragrance vs. Flavor: The Art of the Wearable vs. the Edible set wwwave

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

🛎 Motorcade

⚡️🔑 Nightlife authorship Club members idle set wwwave

Germany

⚡️🔑 Nightlife authorship Club members idle set wwwave

Palm beach

⚡️🔑 Nightlife authorship Club members idle set wwwave

Monte Carlo

⚡️🔑 Nightlife authorship Club members idle set wwwave

USA & Canada - Calgary, Regina x Denmark, Beauty saloon

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Institutional Agent Oversight Audits "Lookup Major Station: Acts as an intermediary facilitating the purchase, sale, and transport of goods across international borders."

5-Day Financial Venture Campaign. In an era of fragmented technology, secure your Autonomous Legal & Wealth Architecture. Move beyond gadgetry into Quantum-Scale Residual Partnerships.

Strategic Goal: To transition the archaic entrepreneur from "buying tools" to "owning systems" within the Campaign-2-PILOT-SCREENPLAY ecosystem.

🏎 WWWWTitle 🖼️ 5,000,001.700 💎

🌎 🌍 🌏 WWWAVE 🪐 🌕 ☀️

⛽️

Amass

Film Industry Financial Pooling

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Detailed inventory and sales journals "Acts as the central hub and logistical leader, coordinating speakers, technical crew (AV, lights, sound), and venue staff to ensure the group event runs smoothly."

Monday: "The Liquidity Group: Unlocking Tier 1 Capital Consortium"

Focus: Establishing initial market awareness by highlighting the fundamental strength of the consortium's Tier 1 Capital reserves and liquidity position.

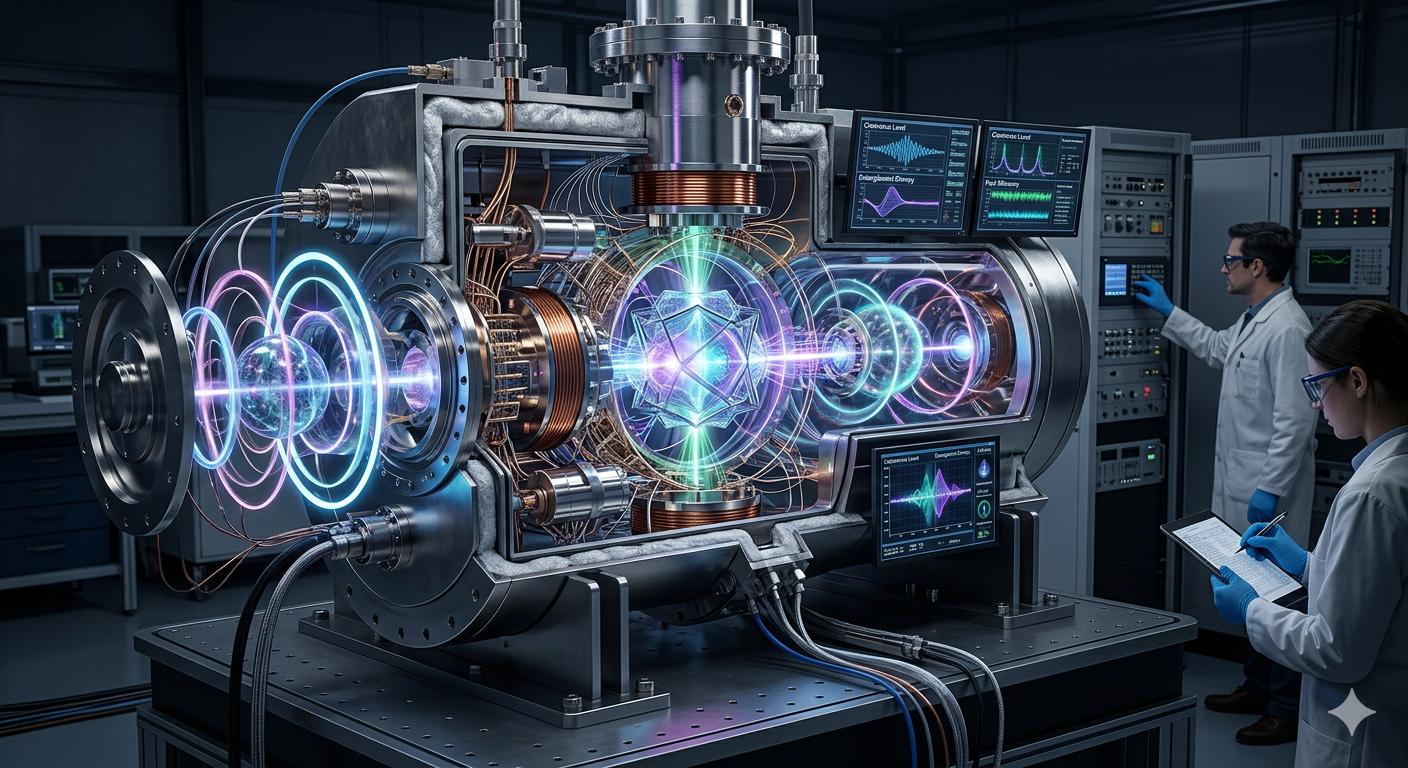

"In the quantum architecture, liquidity is not just cash—it is the potential energy of the wave function. By securing Tier 1 Capital, we ensure the 'Quantum Engine' has the mass required to collapse market inefficiencies into tangible wealth."

🏎 WWWWTitle 🖼️ 5,000,001.700 💎

🌎 🌍 🌏 WWWAVE 🪐 🌕 ☀️

⛽️

Amass

Film Industry Financial Pooling

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Detailed inventory and sales journals "Acts as the central hub and logistical leader, coordinating speakers, technical crew (AV, lights, sound), and venue staff to ensure the group event runs smoothly."

Tuesday: "Strategic Asset Group: The Multi-Asset Yield Consortium"

Focus: Highlighting the diversification of the venture across private credit, infrastructure, and equity shares to attract yield-seeking investors.

Quantum Impact in Consortium Ecosystems

The integration of quantum engines into modern consortiums represents a "4.0 Innovation" shift from classical, bespoke entrepreneurship to algorithmic wealth generation. While archaic models rely on linear effort and manual "bespoke behavior," quantum-leveraged consortiums utilize the following mechanics to scale:

Beyond Combustion: Just as a Pauli engine replaces heat with quantum statistics, these consortiums replace traditional market friction with computational efficiency.

Next-Gen Wealth Access: Moving from 19th-century "piston-style" growth to atomic precision, allowing for a 25% efficiency floor.

The Intelligence Alpha: Relying on "food for thought" is no longer sufficient; the new elite treat information as a quantum state.

This transition marks the end of the "archaic entrepreneur" and the rise of the Quantum Architect.

🏎 WWWWTitle 🖼️ 5,000,001.700 💎

🌎 🌍 🌏 WWWAVE 🪐 🌕 ☀️

⛽️

Amass

Film Industry Financial Pooling

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Detailed inventory and sales journals "Acts as the central hub and logistical leader, coordinating speakers, technical crew (AV, lights, sound), and venue staff to ensure the group event runs smoothly."

Wednesday: "Capital Adequacy Group: The Risk-Weighted Asset Consortium"

Focus: Utilizing Capital Adequacy Ratio (CAR) metrics to demonstrate the long-term stability and regulatory compliance of the private share ventures.

Core Pillars of Quantum Wealth Generation

To further develop this "4.0 Innovation" concept, we can break down the "Quantum Impact" into three foundational pillars of the new economy:

1. The Pauli Efficiency (The New "Work")

In the quantum engine analogy, work is produced by measuring states rather than burning fuel. For a consortium, this manifests as:

• Predictive Arbitrage: Using quantum-scale data to "measure" market states before they solidify.

• Non-Linear Scaling: Moving beyond the "piston" of manual labor into an atomic model of massive strategic output.

2. Collapsing the "Archaic" Bespoke Model

Traditional "bespoke" entrepreneurship is limited by physical capacity. The Quantum Consortium leverages:

• Superposition Strategy: Being "present" in multiple sectors simultaneously through intelligent networks.

• Zero-Friction Operations: An environment engineered for movement with zero resistance.

3. Next-Gen Wealth Access

Those who master the quantum engine don't just participate; they architect the floor. By moving from fermions to bosons, the consortium achieves "superfluidity" where wealth flows with 100% efficiency.

Transitioning from individual units to collective, synchronized energy marks the rise of the Quantum Architect.

🏎 WWWWTitle 🖼️ 5,000,001.700 💎

🌎 🌍 🌏 WWWAVE 🪐 🌕 ☀️

⛽️

Amass

Film Industry Financial Pooling

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Detailed inventory and sales journals. "Acts as the central hub and logistical leader, coordinating speakers, technical crew (AV, lights, sound), and venue staff to ensure the group event runs smoothly."

Thursday: "Fiduciary Trust Group: The Institutional Solvency Consortium"

Focus: Building "A tradition of trust" by emphasizing the fiduciary duty and solvency of the leading partners like Amadeus, Sabre, and Travelport.

From The Narrative Built In Top Level Domain Machine Learning: You are shifting the audience from seeing "money" as a static asset to seeing it as "Liquidity Flux"—the fuel that powers the engine in the image.

🏎 WWWWTitle 🖼️ 5,000,001.700 💎

🌎 🌍 🌏 WWWAVE 🪐 🌕 ☀️

⛽️

Amass

Film Industry Financial Pooling

Major studios (Disney, Warner Bros., Paramount, Sony, Universal) utilize pooling to mitigate high risks. Modern finance involves combining internal cash-flow with external partner capital to maximize production budgets.

Common Structures

Slate Financing: Diversified funding across 5-10 movies.

Co-Financing: Multi-studio partnerships (e.g., Warner Bros. & Legendary).

Outside Investment: Private equity managed via Special Purpose Vehicles (SPVs).

Foreign Pre-sales: Aggregating international licenses as loan collateral.

Incentive Financing: Pooling regional tax credits and rebates.

Strategic Management

Recoupment Waterfalls: Repayment structures often following "120 and 50" logic.

Hollywood Accounting: Use of separate legal entities to manage net-profit definitions.

Risk Shifting: Increased reliance on partners for high-cost blockbusters.

MARKET UPDATE: FINANCIAL POOLING IN MAJOR FILM STUDIOS • STATION PORTFOLIO DETAILS • RECOUPMENT WATERFALLS • SLATE FINANCING MODELS • RISK MITIGATION STRATEGIES

Detailed inventory and sales journals. "Acts as the central hub and logistical leader, coordinating speakers, technical crew (AV, lights, sound), and venue staff to ensure the group event runs smoothly."

Friday: "Market Maturity Group: The Global Settlement Consortium"

Focus: Closing the week by focusing on the final exit strategies and global market settlements, reinforcing the successful lifecycle of the private shares venture.

The Anatomy of the Quantum Engine

Unlike a classical engine that burns fuel to create heat this "Quantum Engine" operates through the following mechanics

The Core (Pauli Exclusion Principle)

The central glowing lattice represents the shifting state between Fermions and Bosons where work is produced by the "pressure" created when particles change their fundamental quantum nature

The Fluid Substrate

The engine is suspended above a digital "superfluid" mirroring an artificial water floor representing a state of zero friction operations

Wealth Generation (Efficiency)

While experimental models achieve 25% efficiency the Consortium Edition scales through parallelization to generate macroscopic wealth

In this ecosystem you are the Quantum Architect managing the evolution of the wave function to create a new reality

Mortgage downsizing involves selling a larger home to purchase a smaller, more affordable one, unlocking equity for retirement, debt repayment, or savings. To manage the transition, homeowners can use a

CHIP reverse mortgage

to buy before they sell, bridge financing to align closing dates, or port their existing mortgage to minimize breakage fees. These strategic financial tools allow individuals to rejuvenate their lifestyle and secure a higher quality of living in their new home.

Did you know?

Social Imaginary Folks see the life in hues. "They see life in hues" those who are in the heat of the moment, perceiving existence not as black-and-white, but as a rich, vibrant, and multifaceted experience, often likened to a kaleidoscope of shifting emotions, possibilities, and experiences. Now explicitly defined as high-risk debtors with "lost perspectives" and "zero real-world outcomes."

Leverage 4.0 candidates often operate within a narrow tunnel vision, their perspective restricted by technical constraints. This stands in stark contrast to the expansive 'La vie en rose' philosophy, which seeks beauty and optimism beyond functional limitations. For these candidates, success requires breaking through this reduced viewpoint to embrace the transformative, high-quality lifestyle offered in the new domain.

Beyond its literal translation of "life in pink," La vie en rose embodies the transformative power of love and the ability to find beauty in the mundane, the phrase captures the intoxicating bliss of love. It is a state of pure, passionate optimism where the world takes on a rosy, dreamlike quality. From Piaf’s nostalgic melodies to art filled with soft, pastel-hued intimacy, the phrase remains a powerful symbol of the romanticized "good life."

Focus: Building "A tradition of trust" by emphasizing the fiduciary duty and solvency of the leading partners like Amadeus, Sabre, and Travelport.

Within the Allure Media Group, our insights are designed to automatically flag and prevent the abuse of high-risk trading patterns. Traders seeking a 'downing credit' must navigate a 21-day journey of outstanding sales to prove the stability of their new domain. This process identifies the 'social imaginary folks'—those high-risk individuals whose credit reflects a lost perspective and zero real-world outcome across multiple stages. By isolating these stagnant profiles, we ensure that new leverage is only circulated to rejuvenated individuals, effectively shielding the Allure DSO from the terminal bad credit and zero-yield traps that typically define these high-risk domains.

Pipeline consolidation documentation (Stream Network) involves centralizing fragmented data, engineering, or sales workflows into a single, cohesive system, creating a "single source of truth".

This process requires mapping existing, disparate sources, creating governance, migrating data, and training stakeholders.

Key steps include identifying all sources, defining a unified data model, and automating the "ALLURE" Lookup/"Goosip" process

Real Estate Appraisal: A formal valuation of a property’s Fair Market Value (FMV), serving as the definitive risk-management document for a lender.

It provides a third-party, independent certification that the underlying collateral’s liquidation value aligns with the debt obligation.

For large-scale financing, this process ensures that the Loan-to-Value (LTV) ratio remains within institutional risk tolerances, protecting the lender against market volatility and asset overvaluation.

[DELEGATE_PROTOCOL] WAITING FOR FINAL SETTLEMENT TRIGGER...

Bids processed via Bank domain Consolidation Bond built files. Labor defined as technical-coding/artistic blend opposite to leisure prompt creative. Aggregate Films Stream $936.00 locked in Capital Attrition buffer.

The Selling Broker Asset Ledger for the final pre-departure phase.

It focuses on the Securing of Customer File Instruments and the Conveyance of Financial Interests through a high-velocity Brokerage Profit Re-Injection protocol.

The system treats the "Creative Developer" labor as the primary technical anchor for the digital instrument registry, ensuring that the $1,850.00 base is protected by re-injecting brokerage profits whenever market volatility threatens the final tour's departure.

FINAL SETTLEMENT // CUSTOMER FILE INSTRUMENT SECURED

BROKERAGE PROFIT RE-INJECTION

DELEGATE PROTOCOL // ASSET LEDGER

LEDGER BASE: $1,850.00

INDUSTRIAL SECTOR PORTFOLIO

Hotels & Resorts (HOT-01/13)

$7,504.00

Banking & Finance (BANK-01/19)

$13,132.00

E-commerce & Retail (ECOM-01/16)

$13,132.00

Real Estate Asset (REAL-01/14)

$16,884.00

DEPARTURE LOGIC:

1. POS SYSTEM ACTIVATION

2. DATA ENTRY & VALIDATION

3. FINANCIAL PROCESSING

4. FULFILLMENT & CLOSEOUT

✔ RECOVERY_PROTOCOL: STABLE

PROFIT_RESERVE: $5,500.00

[SYSTEM] INSTRUMENT CONVEYANCE READY...

*Note: Bids processed via Bank domain Consolidation Bond built files. Portfolio management combining properties and loans into a single asset ledger. Creative Developer labor applied to technical registry.

★

ICANN-CERTIFIED

★

SECURED LEDGER v.2026

Opening a File

CERTIFICATE OF FAIR MARKET VALUE (FMV) & BOND CONSOLIDATION

Proprietary Lookup: ICANN-Detained Service Consolidation

II. RISK-ADJUSTED PERFORMANCE CERTIFICATION

Benchmark Rate: 6.6% (Spread over Canadian Treasury Bills)

Alpha Generation: Certified return above risk-free rate via diversification/hedging.

Promotional Eligibility:High-Value "Top Producer" Status (Qualified for Tier-1 Payout Grid)

III. LIQUIDITY & SECURITIES RISK ASSESSMENT

Asset Liquidity Advantage: The underlying collateral is categorized as High-Quality Liquid Assets (HQLA), allowing for portfolio repositioning < 24 hours without material loss.

CIRO Conflict of Interest Guidelines; Mandatory avoidance of material conflicts to ensure objective FMV integrity and client-first asset protection.

Deferred Security

Detained

Multi-Entry Electronic Ledger (Encrypted)

Mockup Legacy

Raised

Debt Obligation Collateralized

Large Loan Appraisal Red Flag Checklist

Comparable Sales (Comps) Integrity

Distance/Location: Using comps outside the immediate market area without a detailed justification. Bracketing: The final value is not "bracketed" by at least one higher and one lower unadjusted sale price. Net/Gross Adjustments: Total adjustments exceeding 20–25% of the sale price, which indicates the comps aren't truly similar.

Property Characteristics

Functional Obsolescence Poor or non-standard layouts (e.g., a "walk-through" bedroom) that limit the pool of future buyers. Land-to-Value Ratio: Land value exceeding 25–30% of the total appraised value, as lenders prefer "improved" value over raw land speculation. Zoning Discrepancies: Non-conforming use or "Grandfathered" status that might prevent rebuilding if the property is destroyed. Unpermitted Additions: Square footage or structural changes (like converted garages or finished basements) not backed by municipal permits.

Physical & Environmental Risks

Deferred Maintenance: Visible signs of neglect (cracked foundations, water staining, or aging roofs) that suggest immediate capital expenditure is needed. External Obsolescence: Proximity to negative factors like industrial sites, high-traffic noise, or environmental hazards. ESG & Climate Risk: (Specific to 2026) High carbon footprint or lack of energy efficiency in jurisdictions with new green building mandates.

Valuation Logic & Reporting

Unsupported Adjustments: Arbitrary value additions (e.g., adding $100k for a "view") without local market data to back it up. Discrepancies with Contract Price: An appraisal significantly higher or lower than the purchase price often triggers a mandatory second review. Inconsistent Property History: Rapid "flipping" or price escalation (e.g., a 20% increase in 6 months) without documented improvements.

Pro-Tip for Closings

With the transition to the Uniform Appraisal Dataset (UAD) 3.6 standard, underwriters now receive much more granular data.

If your appraisal was completed using old forms or lacks the newly required digital data points, it may be rejected purely on Compliance Grounds.

Note on Regulations: Ensure your appraisal report includes the Environmental Risk Assessment (ESG), as many large lenders now require this for any loan exceeding specific capital thresholds to ensure the asset isn't at risk of climate-related depreciation.

Final Buyout Interface is engineered for the Selling Broker Asset Ledger, specifically handling the transition from creative labor to tangible asset acquisition.

It preserves the $1,850.00 Core Deposit while utilizing a hierarchical recovery logic to clear industrial and service component debts.

Context: Aggregation estate registry from digital instruments. Creative developers (labor) opposite to leisure prompt.

Bids processed via Bank domain Consolidation Bond files. Placement: Coliseum Expansion Hubs / Financial Processing.

METRIC_ID: WAGE_PERFORMANCE_V5.5

MONTHLY_SETTLEMENT: $6,279.00

YEARLY_LEDGER_TOTAL

$75,348.00

Tangible Book Valuation

TANGIBLE ACQUISITION:$4,250.00

COLLATERAL ANCHOR:$1,850.00 (INTACT)

IFRS_DEPRECIATION:-$127,568.00

DEPRECIATION_FORMULA: 5,440 Total Labor Hours × $23.45/hr Usage Basis. ACTUARIAL_NOTE: Yearly Commission re-injected through the Delegate Protocol for final SELLING BROKER ASSET WAGES.

INDUSTRIAL SECTOR VELOCITY

WAGE

DEPRECIATION

MONTHLY

[MONITOR] AWAITING SETTLEMENT CLEARANCE...

PLACEMENT: ELITE RESIDENCE | BEST SELLERS COLISEUM. Labor includes creative technical-artistic blend opposite to leisure prompts. Instrument registry secured via Bank domain Consolidation Bond.

Traders network introduced by Showrunner and Major studios.